Fill in some basic personal information.

Special discount: Get 30 days free plus 40% off Lili Smart fee for 3 months

Get 40% off Lili Smart fee for 3 months

Special discount: Get 30 days free plus 40% off Lili Smart fee for 3 months

Get 40% off Lili Smart fee for 3 months

Tracking your cash flow is crucial to assessing the financial health of your business. In this guide, we’ll help you understand how to read and prepare cash flow statements, as well as provide examples and templates to help you get started.

A cash flow statement (CFS) is one of the three primary financial statements (along with an income statement, also known as a profit and loss statement, and a balance sheet) that businesses prepare for a specific financial period, detailing how much cash was generated or used during that period.

When analyzing the financial performance of a business, a cash flow statement provides clarity about the true financial status of a company, at present. While income statements detail how much has been earned or spent in theory, not all transactions may have been settled at the time of the issuance of the statement. A cash flow statement details the actual amount of cash a business has on hand, helping to assess the liquidity of a business, i.e. the amount of cash available to be used, as necessary, which essentially determines how a business operates.

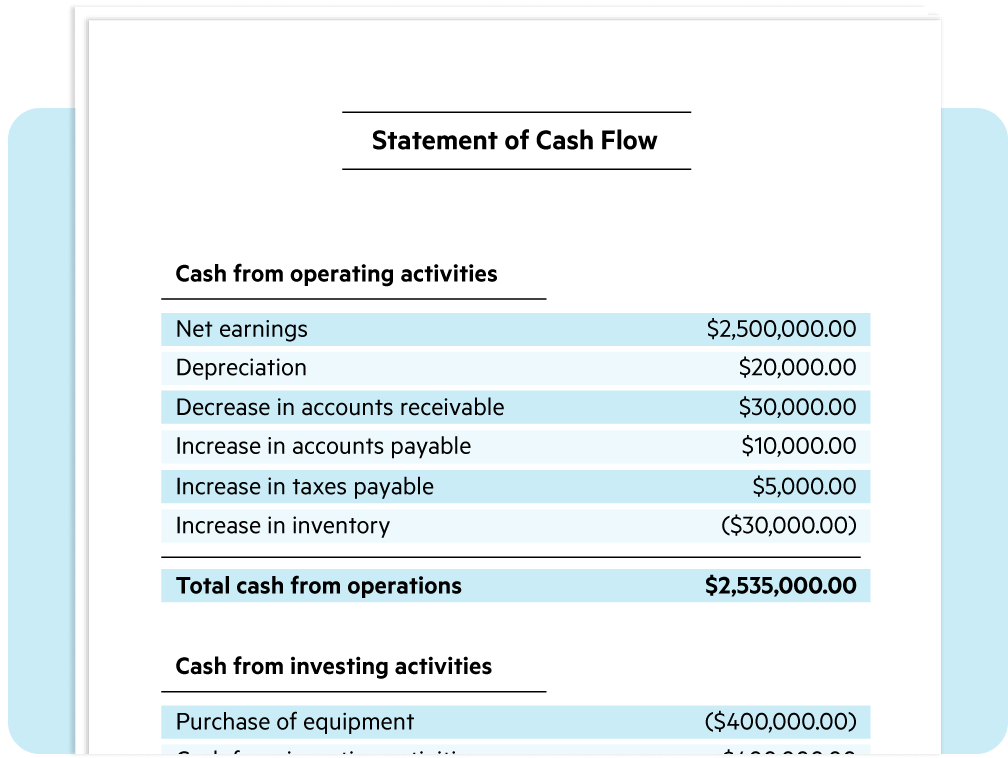

A cash flow statement is structured according to sources of cash: cash from operating activities, investing activities, and financing activities.

Cash from operating activities is often the best indicator of business performance, as these activities denote the day-to-day, primary activities of a business.

For example, if a business sells electronics, cash from operating activities will include cash earned from sales, cash used to purchase the electronics, and other regular expenses like rent, salaries, and utilities.

Cash from financing activities is cash obtained to fund a business, such as from bank loans or external investors.

Cash from investing activities comes mainly from purchasing and selling business assets–specifically assets that increase the long-term economic value of a business.

Examples of business assets include vehicles, computers, real estate, or even intellectual property such as patents and copyrights.

So, if you buy a computer, purchase a patent, and sell a business vehicle, these three transactions and the cash involved will appear on your cash flow statement under cash from investing activities.

To help you get a better idea about determining your cash flow and assessing your business’s liquidity, we’ve prepared a few examples of different cash flow statements, available for download here.

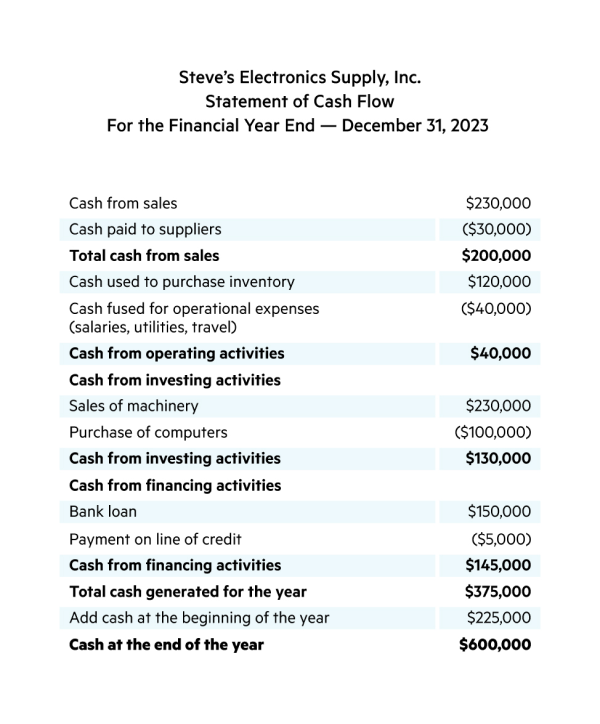

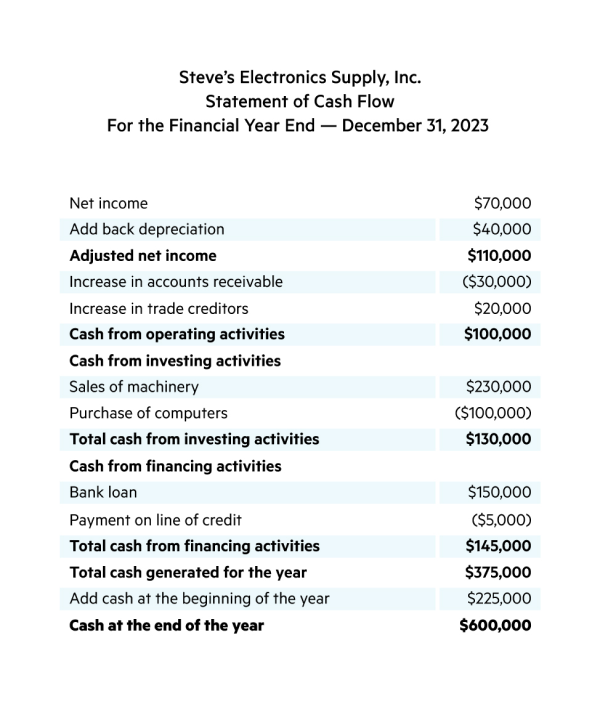

There are two methods of preparing cash flow statements: the direct method and the indirect method.

In this section, we’ll provide an overview of each method and an example statement for each in order to help clarify which method would be more appropriate for your business.

The direct cash flow method relies on cash accounting, meaning cash flow is determined according to when cash is actually received or paid. This method involves calculating cash flow by adding up all cash transaction records, rather than relying on the information provided by balance sheets and income statements.

Usually, the direct method necessitates more work, as a business needs to produce, organize, and track cash receipts for each cash transaction. For this reason, the direct method of preparing a cash flow statement is usually less appealing for small businesses.

The indirect cash flow method utilizes accrual accounting, meaning cash is tallied based on when it is earned rather than when it is received. Accrual accounting relies on balance sheets and income statements, determining cash flow by using net income a defined on the income statement and working backwards to adjust for non-cash transactions.

Most businesses prefer the indirect cash flow method, as it is simpler and less time-consuming than the direct method.

Whether or not a cash flow statement is useful depends not only on the statement’s accuracy, but on the ability of the target audience (e.g. business owner, investor, creditor, etc.) to properly read and understand the statement, especially as to whether cash flow is positive or negative.

Having a positive cash flow means that the cash a business has generated is more than the cash it has spent. Taken at face value, positive cash flow is a favorable outcome. But it’s important to understand that positive cash flow in the short term is not necessarily indicative of long-term positive financial health.

For instance, if a significant portion of cash at present is generated from financing activities like borrowing money, and not from operating activities, this may reveal an underperforming business whose future is in doubt.

Negative cash flow indicates that a business has spent more cash than it has generated in the specified reporting period. While a negative cash flow may appear to be a red flag, it doesn’t always mean a business is in trouble. Just as with positive cash flow, it’s important to dig into the details of a cash flow statement in order to put negative cash flow in the proper context.

Commonly, a startup still establishing itself will naturally operate with negative cash flow for an extended period of time as it relies on funding from external investors and invests in developing its product. In this case, displaying potential for long-term growth and profitability is more important than short-term positive cash flow.

In order to truly understand the insights provided by a cash flow statement, it’s important to pay attention to all details outlined on the statement, not just the bottom line.

A cash flow statement is comprised of the following three components:

Simplify your bookkeeping with instant transaction categorization, and gain clarity about your business’s financial status with income & expense insights and auto-generated financial reports. Make it easier to balance your books with Lili’s Accounting Software.

Live support, 7 days a week

[email protected]

Take a quick tour of the tools inside the Lili account. Banking, bookkeeping, invoicing, and taxes, all in one place.